|

|

Dear Colleague,

In today's edition, we highlight:

- US interest rates must stay high

- UK economy to escape recession

- Japan's inflation target

- The return of industrial policy

- Natural gas security

|

|

UNITED STATES

(Credit: f11photo/AdobeStock)

The United States has proved resilient in the face of the significant tightening of fiscal and monetary policy, but interest rates will have to stay high until late next year to tame inflation in the world’s largest economy, IMF staff said in a statement on Friday.

“Consumer demand has held up well, boosted initially by a drawdown of pent-up savings and, more recently, by solid growth in real disposable incomes,” staff said at the end of the country’s annual Article IV consultation. Prime-age labor force participation has risen above its pre-pandemic peak and real wages have been rising faster than inflation since mid-2022, they added.

But the strength in demand and labor market outcomes is a "double-edged sword", contributing to more persistent inflation, the statement said. While core and headline PCE inflation are expected to continue falling this year, they will remain above the Fed’s 2 percent target throughout 2023 and 2024.

“To bring inflation firmly back to target will require an extended period of tight monetary policy, with the federal funds rate remaining at 5¼–5½ percent until late in 2024.”

|

|

MANAGING DIRECTOR PRESS CONFERENCE

Outlook For United States

|

|

Speaking at a press conference, IMF Managing Director Kristalina Georgieva said that the Fund was keen to see a resolution as soon as possible to the impasse over the debt ceiling. “We are now in the twelfth hour, so a good outcome for the US and the world economy is paramount,” she told reporters. |

|

UNITED KINGDOM

(Credit: IR_Stone/iStock by Getty Images)

The United Kingdom will avoid a recession and maintain positive growth in 2023, but economic activity has slowed significantly since last year and inflation remains stubbornly high, IMF staff said in a statement on Tuesday at the end of a visit to the country.

Growth is forecast to slow to 0.4 percent in 2023, held back by tighter monetary and fiscal policies needed to curb inflation, and the lingering impact of the terms-of-trade shock from Russia’s war in Ukraine and a spike in energy prices. This represents a 0.7-percentage-point upgrade to April’s projection that the economy would shrink by 0.3 percent.

Growth is expected to rise gradually to 1 percent in 2024, as slowing inflation softens the hit to real incomes, and to average around 2 percent in 2025 and 2026.

“Monetary policy will need to remain tight in order to keep inflation expectations well-anchored and bring inflation to target,” Kristalina Georgieva, the IMF’s managing director, told a press conference in London at the end of the annual Article IV consultation.

|

|

JAPAN

(Credit: Gumpanat/iStock by Getty Images)

Japan’s headline inflation reached a four-decade high in February. While lower energy prices have reduced inflation in recent months, underlying momentum in core prices, which exclude fresh food and energy, has also strengthened further, hitting a four-decade high of 4.1 percent in April.

Rapid price gains are rarely desirable, but Japan is an exception after bouts of deflation since the late 1980s and early 1990s. But, as the IMF’s Purva Khera and Salih Fendoglu write in a Country Focus article, there are reasons for hope that the world’s third-largest economy is at a turning point and that the Bank of Japan may finally be able to sustain inflation around its 2 percent target.

The key challenge facing the central bank is how to durably achieve its inflation target without significantly overshooting while safeguarding financial stability. Policymakers must carefully assess the advantages and disadvantages of different approaches as well as potential domestic financial stability implications, as the IMF outlines in the latest staff report.

Writing in the March issue of Finance & Development magazine, Masaaki Shirakawa, Bank of Japan governor from 2008 to 2013, says it’s time to rethink the foundation and framework of monetary policy. Read here.

|

|

FINANCE & DEVELOPMENT

(Credit: Getty Images/Cfoto/Future Publishing)

In the 1990s and 2000s, developing and transition economies opened up their markets and embraced globalization, but now policymakers debate the future of globalization, writes Dartmouth economics professor Douglas Irwin for the upcoming June edition of Finance & Development Magazine.

“Trade interventions are on the rise, in the form of industrial policies and subsidies, import restrictions based on national security and environmental concerns, and export controls to punish geopolitical rivals and ensure domestic supply.” What, Irwin asks, should developing economies do to navigate this new environment? Should they adopt similar policies, turning inward to protect key sectors with subsidies and trade controls?

“Developing economies would be ill-advised to turn their backs on the global economy and give up the idea of supporting exports and acquiring technology from beyond their borders. They still have much to gain from the rest of the world and a lot to lose by returning to the closed-door policies of the past.”

|

|

Many countries have used industrial policy to create global giants like Huawei, General Electric, Volkswagen, and Airbus. The practice of choosing national champions fell out of favor in the 1980s, but in this podcast Yale’s Ruchir Agarwal says rising geopolitical tensions have sparked a renewed interest in industrial policy—which can be a guise for protectionism. |

|

FINANCE & DEVELOPMENT

Coming Soon: June Issue

(Credit: Nataliia Shulga / IMF)

Next week, Finance & Development Magazine will publish its June 2023 issue, entitled Trade, Disrupted.

With the liberal global trading system facing an existential challenge as many countries become increasingly concerned that closer economic integration risks clashing with national security, F&D brings together eminent voices from international organizations, governments, and academia share their views on the global trading regime’s benefits, pitfalls, and opportunities for improvement.

Authors include Benjamin Kett, Caroline Freund, Chad Bown, Christopher Bataille, David Bloom, Douglas Irwin, Jiaqian Chen, Kristalina Georgieva, Leo Zucker, Luigi Zingales, Marijn Bolhuis, Michael Froman, Michele Ruta, Nadia Rocha, Ngaire Woods, Ngozi Okonjo-Iweala, Noah Kaufman, Pinelopi Goldberg, Raghuram Rajan, Ralph Ossa, Roberta Piermartini, Sagatom Saha, Tristan Reed, and many others.

Stay tuned!

|

|

NATURAL GAS

(Credit: Cylonphoto/iStock)

Closer ties allowed Europe to find new natural gas sources after Russia’s supply cutoff, and growing global export capacity can reduce market fragmentation, the IMF's Rachel Brasier, Andrea Pescatori and Martin Stuermer write in a blog.

Natural gas prices can vary dramatically from one place to another because of the complex network of infrastructure needed to transport it. For instance, while pipeline flows to Europe from Russia dropped by 80 percent since mid-2021, sending the continent’s gas prices up 14-fold to a record level in August 2022 and prices for globally traded liquefied natural gas saw a similar jump, LNG prices in the United States merely tripled, remaining several times below Europe and Asia, the authors state.

Expanded LNG export capacity for the United States and other producers may prove crucial to creating truly global gas markets that are balanced across regions. As advanced economies increase reliance on weather-dependent renewable energy from wind and solar, they will likely see critical periods of increased demand for supplemental natural gas to meet power generation needs, the authors write.

“Integrating global gas markets and building needed infrastructure allows prices to stimulate demand and supply reactions in larger, more integrated markets. This helps to buffer global energy markets against supply shocks.”

|

|

|

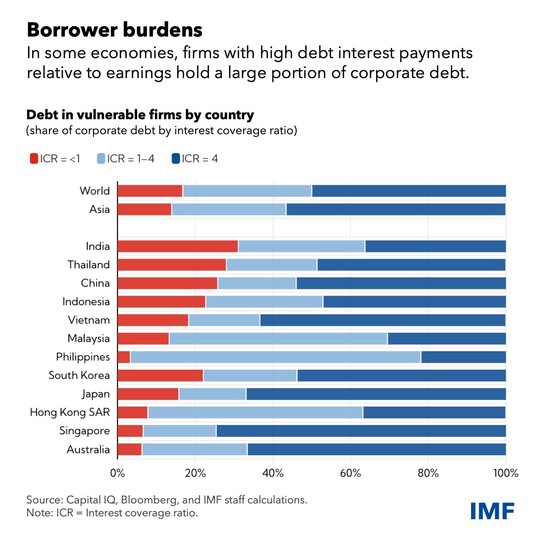

Asia’s increased borrowing in recent decades has augmented the region’s exposure to rising interest rates and heightened market volatility. Even with resilient economic growth, interest payments may exceed earnings as borrowing costs rise, reducing firms’ ability to service their debts. As the Chart of the Week shows, corporate debt is concentrated in firms with low interest coverage ratios. When this ratio, a measure of how much corporate earnings can cover debt interest payments, is below or close to 1, a firm may become unable to service its debts.

|

|

Weekly Roundup

FRAGMENTATION

Talk about fragmentation is not just rhetoric, and the early signs of fragmentation are already taking root, Gita Gopinath, the IMF’s first deputy managing director, said on Thursday. “These changes have ushered in the beginning of a new paradigm in the global economic order—one that shifts away from decades of global economic integration and in which inward- and alliance-oriented policies are gaining traction,” she told a conference, underscoring three areas in the world economy where change is evident already. Read the speech.

EUROPE

Declining energy prices will not be enough to bring Europe’s inflation back to central bank targets, with headline inflation expected to remain high at 5.6 percent in advanced economies and 11.7 percent in emerging economies this year, Alfred Kammer, director of the IMF’s European Department, said on Friday. “To address today’s high inflation, we need tighter monetary policy for longer, until inflation is on a firm path toward target,” Kammer said in a speech during a visit to Montenegro.

SRI LANKA

The IMF’s Sri Lanka mission chiefs Peter Breuer and Masahiro Nozaki spoke to Newsfirst’s Faraz Shauketaly about the country’s IMF-supported program. How will the program will help the economy? What reforms are expected? What is the IMF doing to protect the poor and vulnerable? Watch the interview.

STAFF PAPER

Extended periods of ultra-easy monetary policy in advanced economies have rekindled debate about “zombification” of stricken companies. A recent IMF staff paper finds that recessions are a critical factor in the rapid increase in the number of zombie firms. The authors say that expansionary monetary policy can help reduce zombification when interest rates fall to the lowest level possible (the so-called zero lower bound), but monetary policy that is too accommodative for extended periods is associated with a higher probability of zombification.

STAFF PAPER

Economic news from the United States, and not just monetary policy, affects financial conditions in emerging markets, a recent IMF staff paper shows. News about US employment has the strongest effects, followed by news about economic activity. News about inflation has only limited effects. A key channel of international transmission of US economic news appears to be the risk perceptions or risk aversion of international investors. Some of the transmission of economic news occurs independently of the US monetary policy reaction.

|

|

MAY 30, 6:45 PM ET - MAY 31, 5 PM ET

The Peterson Institute for International Economics hosts a joint conference with the IMF featuring keynote speeches from Gita Gopinath, first deputy managing director of the IMF, Heather Boushey, member of the White House Council of Economic Advisors, and Lawrence H. Summers, Harvard professor and former US treasury secretary.

|

|

Thank you again very much for your interest in the Weekend Read! Be sure to let us know what issues and trends we should have on our radar. |

|

|

|

|