Debt collectors re-evaluate medical debt furnishing in light of data integrity issues

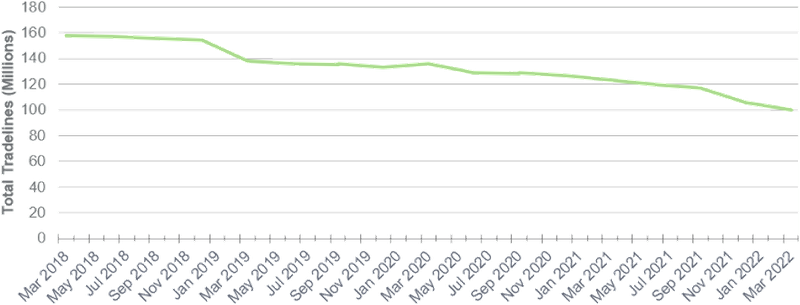

A new CFPB report estimates that medical collections tradelines declined by 37 percent between 2018 and 2022. “Market Snapshot: An Update on Third-Party Debt Collections Tradelines Reporting” also found that medical debt constitutes a majority (57 percent) of all collections on credit reports. This decline, as well as insights from CFPB market monitoring, suggests that debt collectors are moving away from reporting (or furnishing) medical bills to credit reporting companies, resulting in fewer medical tradelines on consumer credit reports. This decline may be partly explained by structural dysfunctions in medical billing and collections, which increase the risk that debt collectors will not meet their legal obligations.

Figure 1: Number of Medical Debt Collections Tradelines, 2018 – 2022

Furnishing medical debt is on the decline, in part due to structural challenges that can result in false and inaccurate information

Most debt collectors collecting on unpaid medical bills do not have timely access to the healthcare providers’ billing and payment information. As a result, debt collectors may be unable to verify whether the medical bills they are collecting on are consistent with healthcare providers’ records, much less verify the underlying accuracy of the bill. Further, unpaid balances on medical bills can and often do change as a result of insurance adjustments or financial assistance, sometimes referred to as “charity care.” In addition, recent media coverage and analysis of complaints received by the CFPB have shown widespread errors, including instances of patients being charged for care that was never received or that should have been covered by insurance. This exacerbates existing concerns about any data disconnects and shows the need for rigorous quality control.

If debt collectors rely on outdated or inaccurate data when they furnish medical billing information to credit reporting agencies, they can cause serious consumer harm and violate the law. These structural barriers to accurate billing, collections, and reporting of medical bills contribute to the higher rates at which medical bills are disputed. These issues also make it harder and more expensive for debt collectors to accurately furnish medical tradelines and exposes them to greater litigation and compliance risks. CFPB market monitoring indicates that some debt collectors are moving away from furnishing medical collections information to credit reporting companies in part due to their concerns about data integrity and their ability to comply with the Fair Credit Reporting Act, including dispute processing.

Inaccurate medical debt tradelines harm patients and the consumer reporting ecosystem

Despite these concerns regarding structural dysfunction and inaccuracy and debt collectors’ ensuing potential liability, medical bills still make up a majority of all furnished tradelines. As of 2021, CFPB research estimated that there was approximately $88 billion of medical bills on consumer reports. Many patients and their families continue to be coerced into paying invalid, unverified, or inaccurate medical bills by the threat of credit reporting. Inaccurate tradelines on consumer reports can prevent patients and their families from accessing the credit they need for housing or employment and can interfere with doctor-patient relationships.

CFPB research shows that medical debt is less predictive of someone’s ability to repay future bills than other tradelines appearing on consumer reports. The data inaccuracies present in medical debt as it is reported can pollute the quality of consumer data and erode the utility of the broader credit reporting ecosystem.

Despite recent industry announcements, patients and families are still vulnerable

Because medical tradelines are more likely to contain errors and less predictive than other kinds of debt, the Federal Housing Finance Authority , other federal agencies , and the White House, as well as the largest nationwide credit reporting companies and VantageScore all took recent actions to reduce the role of medical debt in determining credit access. These changes are important steps, but they won’t solve the structural data integrity issues affecting remaining medical debt tradelines.

Debt collectors are responsible for ensuring the accuracy of debt they collect or furnish, as well as for addressing consumer disputes adequately before continuing to collect. A lack of data integrity in medical billing can result in violations of both the Fair Debt Collection Practices Act and the Fair Credit Reporting Act. This significant liability risk may well have played a role in the significant reduction in the furnishing of medical bills to consumer reporting agencies in recent years.

Given its impact on the lives of patients and families, the CFPB is closely examining medical billing and collections practices. We have published research that explores the impact of medical collections on credit access, issued guidance affirming the legal responsibilities of industry actors, and analyzed industry changes for how they will impact consumers. Through this body of work, we have taken a particular look at the consumer harms presented by furnishing medical debt information and considering medical debt when determining someone’s credit risk. The data integrity challenges discussed in this blog post should be a matter of concern for all those who rely on the consumer reporting system.

As our work on medical debt progresses, we will continue to examine the role that medical bills play in the credit reporting system and the actions of debt collectors in collecting medical bills.